Recently, we hosted an exclusive breakfast at the amazing Leadenhall Building in London with a group of senior insurance underwriting leaders and their data specialists. The session was oversubscribed (a clear signal that AI in underwriting is no longer a theoretical discussion), and the business is ready for change and is embracing it.

What followed was an open discussion about where AI is now (co-pilot, some submission digestion, and two production use cases) and also how it can help the Underwriter process.

The real question isn’t “Will AI replace underwriters?”

The question is either:

“How do I write more business without necessarily adding more underwriters?”

or

“How do we speed up the underwriting and quotation process by automating the non-underwriter tasks of data collection, centralising data, and giving the underwriter everything they need to get to a judgement?”

One theme resonated throughout the morning: traditional underwriting systems were built to force binary decisions: yes or no. But underwriting has never been binary; it’s far more about personal judgements.

It’s “yes, if…”

It’s “depends on…”

It’s “maybe, but…”

That nuance is what makes good underwriters good. Systems need to aid them with those decisions by giving them everything they need.

The cost of the binary system

Many insurers still operate on systems designed to simplify decisions for governance and auditability:

- Rules-based engines

- Decision trees

- Hard-coded thresholds

This means that:

- Exceptions escalate

- Underwriters work around the system

- Potentially profitable submissions time out

- Capacity is consumed by data gathering rather than judgment

Many submissions fall outside the automatic “yes,” and the question becomes: “How many of those could become profitable businesses with better context?”

That’s the Decision Gap.

What leading insurers are doing differently

The most forward-thinking insurers aren’t trying to remove underwriters from the equation. They invest in platforms that:

- Ingest 100% of submissions automatically

- Enrich data from multiple internal and external sources

- Triage by value, not urgency

- Surface relevant risk and portfolio insights instantly

- Provide AI-assisted recommendations, with a human making the final decision

The result? Underwriters spend less time in spreadsheets and data gathering and more time applying judgement.

This increases speed, improves throughput, and efficiency is gained (In fact, Coforge cited an example where an Underwriter group managed to 3x their submissions through their use of automated AI workflows).

From experimentation to production

Everyone has played with ChatGPT, and a lot of the group had some kind of “desktop” AI assistant. But the take-up of agentic workflows, especially, was very light.

The shift now is from pilot projects to enterprise deployment – securely, governably, and with full auditability. AI must sit within the integration layer of the business, not as a standalone tool.

That’s where we see the market heading: AI agents working alongside underwriters, embedded within core workflows, governed like any other enterprise system.

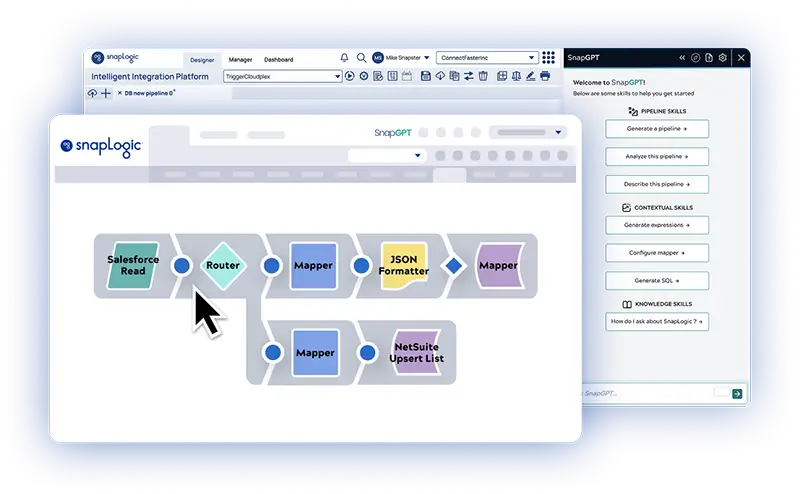

The underwriter’s desktop of the future

We demonstrated what this could look like in practice:

- Zero manual submission entry

- Automated data enrichment

- Real-time policy rule evaluation

- AI-generated summaries and recommendations

- Human confirmation in minutes

The commercial test

Ultimately, the commercial test is simple:

Does your platform increase the percentage of “No” and “If” decisions that become “Yes”?

If it doesn’t, it’s not worth doing.

The appetite in the room made one thing clear: insurance leaders aren’t debating whether AI will change underwriting. They’re focused on how quickly they can implement it in a way that drives measurable commercial outcomes.

Finally, our approach was validated by a recent report by McKinsey. The synopsis is that as generative and agentic AI advances, the following is likely:

- Routine tasks like data ingestion, document generation, and initial risk evaluation will be largely automated

- More sophisticated AI could handle end-to-end workflows for straightforward risks (e.g., auto-renewals or simple commercial lines) without constant human oversight.

- Human underwriters will focus more on exceptions, complex judgment, relationship management, and model oversight

Underwriting’s next era is agentic

The future of underwriting is defined by agentic workflows, with AI agents embedded directly within the integration layer, governed and fully auditable. This shift will power the Underwriter Desktop of the Future, eliminating manual submission entry, providing real-time risk evaluation, and delivering AI-assisted recommendations in minutes.

For insurance leaders, the singular mandate is measurable commercial outcomes: demonstrably increasing the percentage of profitable submissions that move from a complex “No” or “If” decision to a definitive “Yes.” The time for debate is over; the industry is focused on rapid implementation to usher in the new era of AI-first underwriting.

Ready to see how SnapLogic powers the Underwriter Desktop of the Future? Request a demo today.